Once you allow your economy to become dependent on extremes of debt, leverage, inequality, legalized looting, monopoly, pay-to-play politics and speculative asset bubbles, a depression is inevitable.

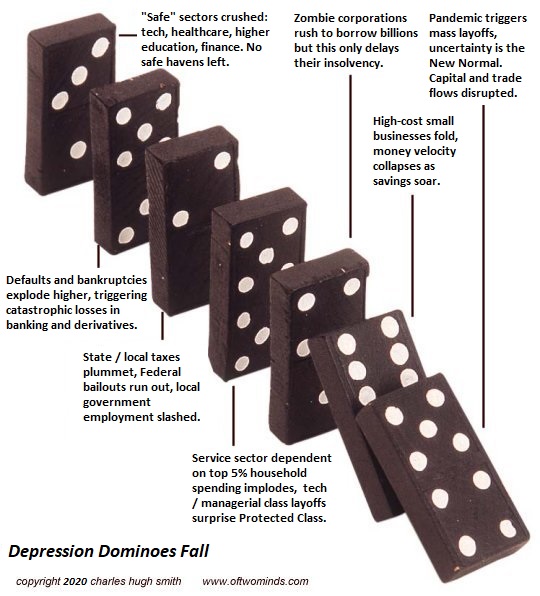

The pandemic lockdown will be blamed for the Greater Depression, but the lockdown only toppled all the dominoes that were already lined up. The lockdown would have been survivable if the economy hadn't been over-indebted, over-leveraged, burdened by insanely high costs, stripmined by greedy monopolies, dependent on stock market fraud, destabilized by extreme inequality, corrupted by political pay-to-play and addicted to speculation.

The apologists always blame depressions on central banks not printing money fast enough, while overlooking the real drivers: debt, high costs and dependence on speculative bubbles. As noted here many times, revenues and income can quickly slide lower, but debt must be serviced regardless of revenues and income.

Once debt payments dominate expenses, any wobble in revenues / income / cash flow triggers default.

Regarding unbearably high costs that only go higher, year after year: as noted here many times, Sickcare Will Bankrupt the Nation all by itself, never mind soaring higher education / student loan debt serfdom, skyrocketing rents, junk fees, taxes, etc.

U.S. Lifestyle + "Healthcare" = Bankruptcy (June 19, 2008)

The truth is the cost of living is unaffordable but we can't even acknowledge this obvious fact because even acknowledging it would threaten the entire house of cards. So instead we play-act as if we believe the bogus "inflation is dead" narratives.

The top 5% technocrat/managerial class have done very well for themselves in the speculative run-up of destabilizing inequality, and since they run the narrative machines, we're swamped with happy stories about the economy, all of which boil down to this absurd fantasy: since I'm doing so well, everyone else must be doing well, too.

Since the top 5% own the lion's share of the nation's productive assets--stocks, bonds, business equity, investment real estate, etc.-- the enormous asset bubbles have greatly boosted their wealth and income. This has enabled the wealthy to service their debt or pay it off. The bottom 95% aren't quite so well-placed to survive a decline in income.

Everyone who was barely keeping their head above water in making their debt payments is already in default or will soon be in default. Since the banks and shadow-banking lenders have gorged on the profits skimmed by loaning huge sums to marginal borrowers, now that these marginal borrowers are defaulting en masse the banks and lenders are about to be crushed by one wave of catastrophic losses after another.

Student loans--already in mass default. Credit cards--the wave is rolling in as we speak. Auto loans--looking like Waimea Bay on a big day. Mortgages--better not to look.

Corporate debt has exploded to unprecedented levels, and this is what will break the financial system. Zombie corporations are rushing to borrow billions of dollars (thanks to the Federal Reserve) but increasing their debt is only doing more of what created their fragility in the first place.

Being able to borrow more to service your old debts is not solvency, it's merely the semblance of solvency. We're in the eye of the hurricane right now, as everyone holds their breath and hopes some sort of magic will make all the debt that has to be serviced every month vanish.

It's worth recalling that every dollar of debt is someone else's asset and the source of their income. So when the defaults and bankruptcies sweep through the financial system, they'll obliterate all the "wealth" of those holding bundled student and auto loan securities, mortgage backed securities, corporate bonds, and destroy the income streams these trillions in debt generated.

All the linked fragilities and dependencies of our economy are like lines of dominoes: one default topples the entire line of dominoes of debt, leverage, derivatives, counterparty risk, credit default swaps and most devastating of all, any certainty that borrowers won't default in the future.

If banks and lenders can't lend with a high degree of certainty, lending dries up and profits collapse, along with the consumer spending that was enabled by the borrowing.

Despite their high incomes and net worth, some consequential percentage of top 5% households bringing in $300,000 a year are one layoff away from default: never mind their pristine 830 credit score; that was last month. Next month,next quarter, next year--all bets are off.

Once you allow your economy to become dependent on extremes of debt, leverage, inequality, legalized looting, monopoly, pay-to-play politics and speculative asset bubbles, a depression is inevitable. The only question is "when," and that's been answered, though nobody wants to hear it: 2020 and beyond.

It didn't have to end this way. If our leadership / Power Elites had acted to reduce all these painfully obvious speculative extremes, dependencies and fragilities and made even modest efforts to limit the exploitation of predatory parasites that generated unprecedented inequality and corruption over the past 12 years, the economy would have been much less brittle / fragile.

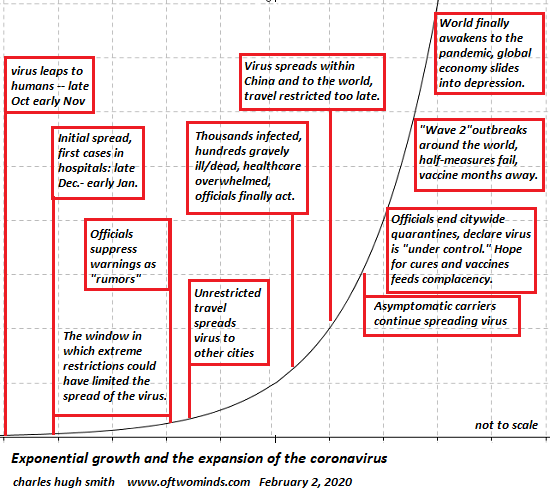

Unfortunately, the pandemic chart I composed on February 2, 2020 is still playing out, increasing uncertainty.

What's the price of systemic fragility and uncertainty? I fear it will be steeper than we're prepared to pay.

Recent Podcasts:

A Reverse Wealth Effect? (41:52)

Audiobook edition now available:

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 (Kindle), $12 (print), $13.08 ( audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print) Read the first section for free (PDF).

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Mike G. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, Robert J. ($50), for your magnificently generous contribution to this site -- I am greatly honored by your support and readership. |