Any economy that concentrates its wealth and income in the top tier is a fragile economy.

There are two structural reasons why consumer spending will not rebound, no matter how "open" the economy may be. Virtually everyone who glances at headlines knows the global economy is lurching into either a deep recession or a full-blown depression, depending on the definitions one is using. Everyone also knows the stock market has roared back as if nothing has happened.

While most financial pundits have accepted that a V-shaped recovery is not possible, few (if any) observers have discussed two factors that will cause consumer spending to crash harder than generally expected:

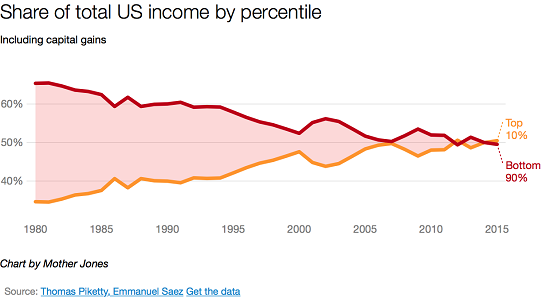

1. The top 10% of households account for about half of all consumer spending, and these are the households that will be most affected by the sharp drop in assets, small business income and the shrinking of heretofore "safe" white-collar jobs in higher education, healthcare, finance, etc.

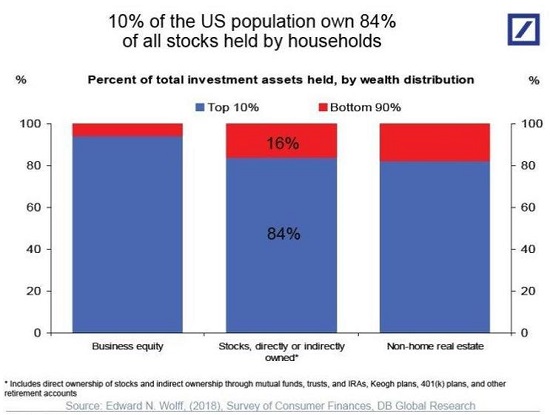

In other words, since the top 10% own roughly 85% of all non-family-home assets (i.e. stocks, bonds, business equity, rental real estate), the decline in the value of these assets and the decline in the income generated by these assets will hit the top 10%, not the bottom 90% who own a tiny sliver of these assets. (see charts below)

Companies are slashing dividends, tenants are not paying rent and family-owned businesses will experience declines in revenues and profits--even those which have yet to feel the consequences.

All of these income streams and assets are owned by the top 10%, and so all these declines in wealth and income will be concentrated in the top 10%.

2. The majority of the wealth owned by top 10% households is held by people 50 years of age or older, and this older cohort that owns most of the wealth and the income streams generated by the wealth are more at risk of Covid-19 than younger people. Surveys have found that people who feel more at risk are much less inclined to start going back to restaurants, musical events, etc., or going on cruises or airline flights.

It's important to note that risk is an internal assessment. Thus the economy can be completely open again but people who feel cautious won't resume their old spending habits, and there is no way to force them to do so.

The data strongly suggests elderly people and those with metabolic issues--obesity, high levels of sugar or cholesterol, and high blood pressure--are at greater risk than healthier people. (Vitamin D and zinc deficiencies may also play a role, as well as general immune response.) I recently saw a statistic that only 15% of the American populace is metabolically healthy. The point here is that a sense of heightened risk is sensible for a great many people, and since the owners of most of the wealth are older, this caution will have outsized impacts on consumer spending.

Combine this with the shrinking wealth and income of the top 10%, and you get a double-whammy reduction in consumption.

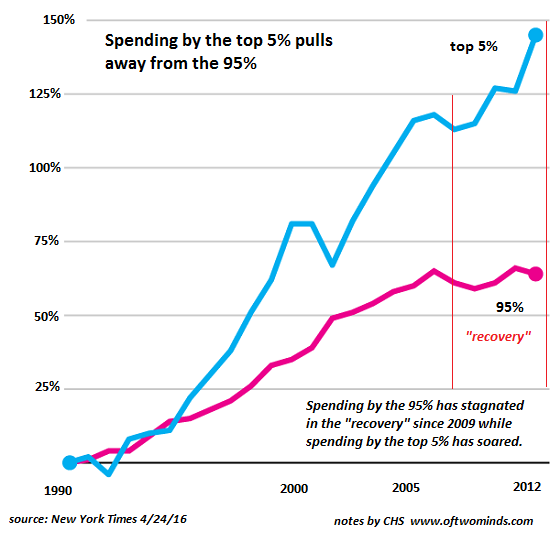

It's also instructive to gauge the enormous asymmetry in what the top 10% spend on services compared to the bottom 90%. The bottom 90% may get their hair or nails done and have the oil changed in their car, but they typically can't afford (or don't need) all the services routinely engaged by the top 10%: dog walkers, CPAs, tax accountants, attendants for elderly parents, piano lessons and other tutoring for children, fitness trainers, career counselors, landscape designers and so on--the list is practically endless.

Once the top 10% are forced to tighten their belts, it won't be Wal-Mart sales that are hit--it will be millions of service providers who depended solely on the top 10% (or top 5%) for virtually all their income.

All the professions that only served the top 10% will be decimated, as they are all inessential. Virtually every one of these tasks can be cancelled, put off into the future, or performed by the household if push comes to shove financially.

The arts and performing arts that depend almost entirely on costly ticket sales to the wealthy and donations from top 5% households will also be decimated. If you attend the symphony, ballet or opera, you know 90%+ of the audience is over 60--the very cohort that will now hesitate to spend lavishly or attend crowded performances.

Based on my admittedly informal observations, I think it's a fair assessment to say that a great many top 10% households are in denial about the financial tsunami that's about to hit them. Since they weren't furloughed like lower-income workers, they have a delusional faith that their incomes, business and wealth will survive the depression intact.

They are looking at the water receding from the bay, leaving all the fish flopping in the seabed, and reckoning that's the worst that will happen. They don't yet understand that the tsunami that's about to roar ashore is not yet visible. The financial wave has yet to hit them, but when it does, they will find:

1. Their unearned/investment income will drop.

2. Tax hikes will be aimed exclusively at the top 10%, further eroding their income.

3. Their services weren't as essential or in demand as they assumed, because they assumed the top 10% that make up the bulk of their customers would resume spending freely.

4. Their assets will decline in value, as the only buyers are other top 10% households, and these declines in wealth and income will create a self-reinforcing downward spiral.

2. Tax hikes will be aimed exclusively at the top 10%, further eroding their income.

3. Their services weren't as essential or in demand as they assumed, because they assumed the top 10% that make up the bulk of their customers would resume spending freely.

4. Their assets will decline in value, as the only buyers are other top 10% households, and these declines in wealth and income will create a self-reinforcing downward spiral.

If assets will lose $10 trillion in value, virtually all of this will come out of the accounts of the top 10%. If investment and business income declines by $1 trillion, virtually all of this will come out of the incomes of the top 10%.

In summary: the vast majority of spending by the bottom 90% isn't discretionary: it's mostly servicing debt (student loans, mortgages, auto/truck loans, credit cards, etc) and essentials (rent, food, utilities, etc.), with modest discretionary spending on fast food and cheap goods.

In contrast, the top 10% spending--almost half of all consumer spending-- has supported a vast number of service businesses, jobs, arts organizations, etc.--entities that receive very little of their revenues from the bottom 90%. As the top 10%'s income crashes, so will their discretionary spending. The older the wealthy household, the more likely they will hesitate to spend as their nestegg is crushed and their caution about crowds endures.

These dynamics are under-appreciated in my view, and so the majority of media commentators and the top 10% themselves are unprepared for the asymmetric impacts on their own wealth, income and livelihood that will sweep ashore later this year.

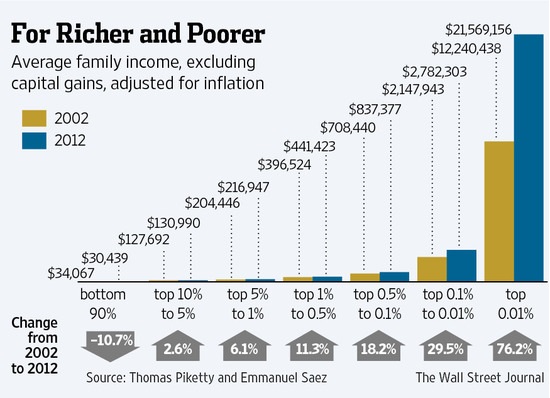

This trend reversal in top 10% spending has been building for some time: Early warning sign of recession? High-wage workers are spending less (11/29/19) "The trend is noteworthy because the top 10% of households by income make up nearly half of all consumption."

Any economy that concentrates its wealth and income in the top tier is a fragile economy.

Audiobook edition now available:

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 (Kindle), $12 (print), $13.08 ( audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print) Read the first section for free (PDF).

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Matthew C. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Tutor ($50), for your magnificently generous contribution to this site -- I am greatly honored by your support and readership. |