The global risk premium has increased dramatically and is increasing in an unpredictable arc. This structural trend of higher risks will reprice everything.

The global economy is changing in fundamental ways, and this is repricing everything: the cost of money/credit, the price of assets, the value of hedges and insurance, and so on. The core driver in all this repricing is risk, for it’s the reappraisal of risk that forces the repricing of everything.

When risk is low and transparent, the risk premium is low and this is reflected in low, stable costs. When risk soars and is difficult to assess, the risk premium rises and this pushes costs higher.

In terms of asset valuations, higher risks reprice assets higher or lower based on the risk profile: what happens to the asset if liquidity dries up in a risk-driven crisis? If credit dries up, what happens to demand for the asset?

Risk tends to be self-reinforcing. If we look around and see everyone else is confident that risk is theoretical rather than real, we stop buying hedges against bad things happening, and we pay a premium for assets that do well in low-risk eras.

But if we see other people getting defensive–selling assets, paying down debt, reducing spending and risk-on investing–then we pull in our horns, too.

What changed?

The global economy began a cycle in the early 1990s of declining risk throughout the system due to these risk-reducing changes:

1. The dissolution of the USSR and the end of the hyper-expensive, heightened-risk Cold War.

2. The flood of low-cost oil as all the super-giant fields discovered in the 1970s began peak production.

3. China emerged as the low-cost “workshop of the world,” enabling 30 years of soaring corporate profits as corporations reduced costs by offshoring production to China.

4. This offshoring boosted profits while deflating the costs of production due to much lower labor costs, lax / non-existent environmental standards and Chinese producers’ willingness to accept razor-thin profit margins.

5. The reduction in global risk and the deflationary impact of Globalization (offshoring and opening new markets) enabled central banks to lower interest rates for 30 years without sparking inflation and private-sector banking/lending to expand credit and leverage, effectively globalizing / commoditizing financial instruments that hedged risks (Financialization).

6. After a decade-long lag (the 1980s), the advances in personal computing, software and desktop publishing finally began generating productivity increases.

7. The economic theology of Neoliberalism was embraced globally. Neoliberalism claims “markets solve all problems” and so the universal solution is to turn everything into a market by reducing regulations and state oversight.

All of these forces tended to restrain prices of commodities, goods and services and reduce systemic risks while expanding markets, financial “innovations” and profits. This created a global “virtuous cycle” in which each dynamic reinforced the others.

This “virtuous cycle” ended in the 2008-09 Global Financial Meltdown, but was papered over for a decade by extreme policies:

1. China launched the largest credit expansion in history (Russell Napier’s phrase) to counter the meltdown

2. The Federal Reserve and other central banks began a policy of financial repression (i.e. centrally managing financial markets rather than let market forces dictate liquidity, price, risk, etc.), leading to Zero Interest Rate Policy (ZIRP) that was effectively negative-rates since inflation continued sputtering along at 1.5% tp 2%.

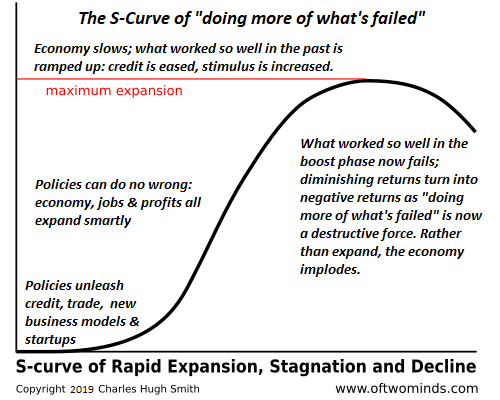

Why did the “virtuous cycle” end? The basic answer is diminishing returns: the returns on any new policy or dynamic such as Neoliberalism, globalization or financialization follow an S-Curve, where the initial returns are stupendous (the boost phase) and then as the dynamics become ubiquitous, the returns diminish until they stagnate. At that point, the system decays unless new more extreme measures are applied–for example, China’s debt to GDP ratio doubling from 140% to 280% and interest rates being suppressed to zero.

Another factor is the cannibalization of domestic markets once globalization had skimmed the easy returns. Financialization starts out looking “innovative” by claiming it can hedge all risks at low cost, effectively lowering the risk of playing financial games to zero. As Benoit Mandelbrot and other explained, this isn’t possible for structural/mathematical reasons (markets are inherently fractal and prone to instability),

As the easy gains diminish, financialization takes assets that were once low-risk and commoditizes them into “instruments” that can be sold globally, suppressing the visibility of risk with deceptive packaging. This is what happened to home mortgages, which went from being highly regulated and low-risk to being poorly regulated /fraudulent and packaged into highly deceptive mortgage-backed securities that masked the true risk–high–behind flim-flam claims of low risk.

As costs rose in China and other producing nations, labor costs began rising, along with higher taxes and some attempts to reduce the choking air pollution and poisoned water/soil that inevitably result from uncontrolled industrialization.

Suppressing the cost of capital/credit to near-zero generated a tsunami wave of borrowed capital, both within the banking sector and the ballooning non-banking (shadow banking) sectors. This low-cost credit was then unleashed into global markets to chase any high-yield investment, which of course means gambling on risky assets while supposedly hedging the bets against losses.

All this financial engineering–ZIRP, cheap, abundant credit, the chase for yield–ultimately depends on liquidity, i.e. the presence of buyers in size to create a market for anyone who seeks to sell an asset. If liquidity dries up for whatever reason–a bank crisis, a market panic, etc.–then sellers run out of buyers and the market reprices the asset at lower and lower levels until buyers emerge. In a collapsing-liquidity market, there are few buyers at any price.

The potential wipeout of “wealth” i.e. asset valuations would bring down the entire global financial system, for all those assets are collateral for the world’s immense mountain of credit/debt.

The evaporation of liquidity in 2008-09 is what former Fed Chairman Alan Greenspan identified as the risk he did not anticipate.

So what changed around 2007-09? Globalization and Financialization moved from “virtuous cycle” to stagnation / decline, policies became more extreme to bury rising systemic risks, and the addition of a billion new workers aspiring to all the commodity-consuming luxuries of the middle class lifestyle soaked up surplus production of oil and other commodities. With surpluses gone, prices had to start rising.

Post-Covid lockdown and recovery, China’s policies changed from “open to the world” and “peaceful rise” to aggressive militarization and territorial claims and the restriction of Chinese society’s access to the outside world.

All of these factors exposed the risks that had been successfully obscured: the risks that global supply chains can break down or be disrupted by geopolitics; the risk that financialization games can blow up; the risk that Neoliberalism failed to suppress risks of fraud and exploitation; the risks that soaring debt outpaces expansion of the real-world economy, generating debt crises, and the risks of extreme policies generating unintended consequences (moral hazard, extreme risk-taking, too much debt, etc.) and blowback (re-industrialization, trade wars, etc.).

On top of these risks, there are now demographic, capital, labor and resource sources of risks. Geopolitical tensions are rising, which is historically typical in eras where essential commodities become scarce and/or unavailable /costly. This is incentivizing re-industrialization, reshoring, friendshoring, etc., all of which are national-security issues aimed at reducing dependency on rivals or risky supply chains.

In effect, the nation-state has to take the driver’s seat from quasi-deregulated markets, the Neoliberal ideal. In reality, deregulated is the happy-story codeword for centrally managed to benefit the few at the expense of the many.

This re-industrialization is also driven by the transition to non-hydrocarbon energy sources, a goal that will require far more capital than most expect even as it underperforms unrealistic expectations. The demand for trillions in new investment will pressure credit for consumption (new homes, vehicles, vacations, etc.), pushing the cost of credit higher regardless of any other conditions.

In the past decade, birth rates in many developed and developing economies have cratered while the workforce ages and enters retirement. Both of these developments mean pension and social welfare programs launched when there where 5 workers for every retiree are no longer sustainable now that there are only 2 fulltime workers for every retiree/recipient of social welfare.

The decline of the workforce also introduces two other dynamics: potential labor shortages and the stagnation of demand, as older people consume far less than new households having children. As marriage rates and birth rates plummet, so do the prospects for consumption-driven economic growth.

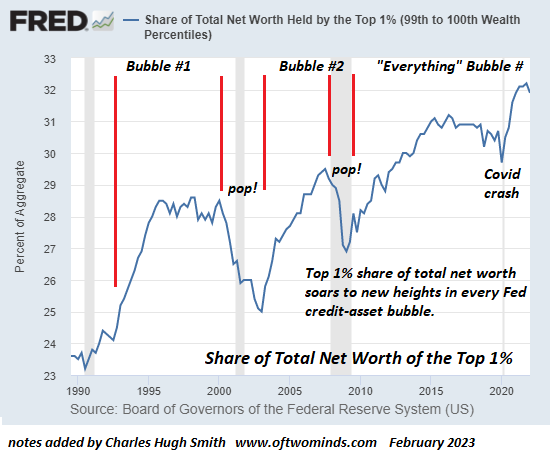

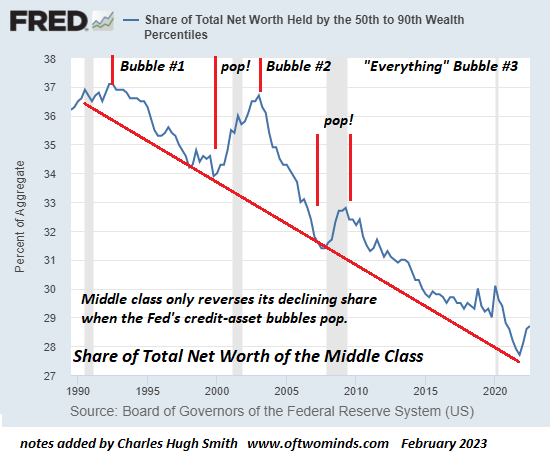

The policy extremes of ZIRP, moral hazard, credit expansion and the chasing of yields has inflated The Everything Bubble which has put the price of housing and vehicles out of reach of the bottom 60% (or in many regions, the bottom 80%) of households.)

This rising inequality erodes social cohesion and fosters an alternative lifestyle in which young workers opt out of the rat race to acquire an upper-middle class income and wealth. This diminishes the pool of potential buyers of all the overpriced assets, further reducing liquidity on a demographic/structural basis.

Simply put, the rising tide of wealth and profits hasn’t raised all boats. The top 5% have garnered the vast majority of the gains in asset appreciation, capital gains and profits. This generates a background of rising risk of social disorder.

On top of all this, 30 years of moderate inflation have reversed into a era of sustained inflation, which despite the hopes of many commentators, will not be transitory. This era of inflation is driven by:

1. Excessive debt levels that can only be managed by inflating the debt down to manageable levels

2. Scarcities of essentials which push prices above what consumers can afford while not being high enough to fund massive new investments needed to increase supply.

3. The cost of capital must rise to reflect the rising risk premium globally.

All the tricks deployed to restore confidence in 2008-09 have reached such extremes that now systemic risk–of default, conflicts, broken supply chains, geopolitical blackmail, scarcities of essential commodities and perhaps the least understood risk, the evaporation of liquidity as credit and buyers of risk-on assets become scarce–is rising dramatically.

These risks are difficult to assess or hedge completely, and the inter-dependence of the global economy and financial system–a tightly bound system–mean risk in one area quickly spreads to the rest of the system.

This structural rise in systemic risks raises costs and changes the risk-reward calculation on every asset.

Take housing as an example. When we’re confident housing will rise 30% every decade like clockwork, we’ll pay today’s prices with the expectation that the house will gain 30% in the coming decade. But as the financial risk premium rises, and we have to factor in the risk that the house might lose 30% of its value going forward, we become wary of paying today’s high price.

As others also become wary, the recognition of risk reinforces itself and as prices drop, our wariness increases and we decide to wait until the risks of further decline become clearer.

The problem with assessing risk is the full risks are never clear until it’s too late.

Everything is being repriced, including risk, the cost of capital and labor and the value of all assets. This repricing is currently modest, but as risks manifest, we can anticipate an acceleration of repricing. If liquidity dries up–buyers for houses and stocks suddenly withdraw from the market–the price declines can be dramatic and self-reinforcing.

In a system maintained by ever-greater extremes, confidence erodes very quickly once the next extreme fails to move the needle. At that point, all bets are off because confidence in the policymakers’ ability to “save the day” vanishes. And once confidence vanishes, so does liquidity. Once markets are illiquid, the problem isn’t limited to the declining valuation–the real problem becomes finding a buyer who will enable you to convert the asset into cash.

The global risk premium has increased dramatically and is increasing in an unpredictable arc. This structural trend of higher risks will reprice everything.

This will generate consequences and opportunities which I discuss in my books

Global Crisis, National Renewal

and

Self-Reliance in the 21st Century.

This essay was drawn from my Weekly Musings Reports sent exclusively to

subscribers,

patrons and

Substack subscribers. Thank you very much for supporting my work.

New Podcast:

Charles Hugh Smith on Getting Ready for a Real Recession (38 min) (38 min)

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

| Thank you, Suzanne S. ($70), for your monumentally generous contribution to this site — I am greatly honored by your steadfast support and readership. |

Thank you, John G. ($5/month), for your most generous pledge to this site — I am greatly honored by your support and readership. |

| Thank you, Allan H. ($10/month), for your outrageously generous pledge to this site — I am greatly honored by your steadfast support and readership. |

Thank you, Daniel T. ($1/month), for your most generous pledge to this site — I am greatly honored by your support and readership. |