Not only will there not be a recovery, but there can't be a recovery, as those brittle extremes have been lost for good.

How did the global economy end up teetering on a precarious financial precipice? To formulate a cogent answer, let's take a whirlwind tour of the history of the global economy 1946-2020.

Before we start the tour, I want to return briefly to my first Musings of the year, which was posted on January 4, 2020, before Covid-19 was officially announced on January 23, 2020. (The Musings Reports are sent weekly to patrons and subscribers at the $5/month or higher level.)

Instability Rising: Why 2020 Will Be Different:

"Economically, the 11 years since the Global Financial Crisis of 2008-09 have been one relatively coherent era of modest growth, rising wealth/income inequality and coordinated central bank stimulus every time a crisis threatened to disrupt the domestic or global economy.

"Economically, the 11 years since the Global Financial Crisis of 2008-09 have been one relatively coherent era of modest growth, rising wealth/income inequality and coordinated central bank stimulus every time a crisis threatened to disrupt the domestic or global economy.

This era will draw to a close in 2020 and a new era of destabilization and uncertainty begins."

The long-term trends set up a row of dominoes that the pandemic has toppled. But any puff of air that toppled the first domino would have toppled all the dominoes of fragility, instability and unsustainable extremes that characterize the global economy.

The whirlwind tour of the global economy's history must include these essential dynamics: energy, currencies, globalization, debt and financialization, which broadly speaking refers to everything that renders finance (borrowing, leverage, speculation) more profitable than actually generating goods and services.

The "glorious thirty" (Les Trente Glorieuses) years from 1946 to 1975 were decades of rising prosperity in the developed world (Europe, Japan, North America) and rapid development in the first tier of developing countries in Southeast Asia and elsewhere. (Decolonized nations and China struggled with political, social and economic turmoil.)

Costs were low for fuel, housing, food, healthcare, education, etc. as rebuilt industrial bases produced lower cost goods and oil/natural gas were cheap. The global currency market was stable as the U.S. dollar was pre-eminent, enabling Japan and Western Europe to sell their goods to America at discounted prices due to the strong dollar. This policy was explicitly designed to strengthen the economies of allies faced with the threat of the Soviet Union's global ambitions.

The "glorious thirty" were also decades of rising wages and affordable, modestly growing credit and low inflation as the money supply expanded more or less in tandem with the expansion of goods and services and credit.

The wheels fell off in the 1970s as the oil-exporting nations muscled energy prices higher to gain a share of the profits, the gold-backed US dollar regime fell to pieces and inflation skyrocketed, generating a previously unknown economic malaise known as stagflation: high inflation plus stagnant growth.

At this same juncture, the external costs of industrial pollution finally came due, and global competition from lower-cost nations (helped by currencies that traded at deep discounts to the US dollar) crushed inefficient industries in the U.S. and Europe.

The 1980s saw a resurgence of growth, but with a different mix of sources. Demographically, the global postwar Baby Boom generation entered their highest productivity and spending years, boosting global demand, the supermassive new oil fields discovered in the early 1970s finally came online (Alaska, North Sea, West Africa), dramatically lowered the price of oil while soaring interest rates crushed inflation and wrung bad debt out of the developed economies, Developing nations that had struggled in the 1970s finally found their footing (India, China, South America, etc.)

The steep investment in reducing pollution began paying off and the first wave of financialization boosted mergers, buyouts and asset prices.

The 1980s was capped by the decline and fall of the Soviet Union, eliminating the costly military rivalry of the Cold War, and the collapse of Japan's massive credit/asset bubble in 1989-90--a warning sign that was ignored as a one-off.

The 1990s continued the trend of global growth, aided by low inflation, cheap energy, expanding globalization and the mass commercialization of the Internet and computing, as technologies that were once expensive and difficult to use became affordable and accessible.

The Neoliberal ideology --that the way to solve virtually any problem, from poverty on up, is to turn everything into a global market of freely traded labor, capital, goods and services-- became the default global economic faith, with some variations (a market economy with Chinese characteristics, etc.)

The 1990s was capped by the emergence of China as the manufacturing hub of the global economy, a role that was institutionalized by China's acceptance into the WTO, and the bursting of the Dot-Com bubble in March 2000.

As globalization and financialization became dominant forces (the natural result of Neoliberalism), instabilities appeared in currency markets (the Thai baht / Asian contagion of the late 1990s) and asset markets (the Dot-Com stock market bubble). Japan's recovery from the credit bubble collapse faltered, ushering in 30+ years of stagnation, leading to an overlooked social decay with extraordinary demographic and economic consequences that are still playing out.

As the global economy reeled from these instabilities in 1998-2000, central banks flooded asset markets with newly created currency, the goal being to stave off a recession, which burns off bad debt, marginal investments and companies, reducing credit expansion and consumption.

Rather than accept the risks of a conventional business-cycle recession, central banks pushed financialization to new heights--heights which quickly distorted markets.

As a result, the growth of the 2000s was different: in effect, central banks had created a credit/asset-bubble dependent economy, with growth coming not from lowering costs, improving productivity and rising wages, but from speculations in financialized markets.

This was simply the logical extension of Neoliberalism: if existing markets weren't profitable enough, then create new markets for new exotic financial instruments and lower the cost of borrowing to spur consumption and investment.

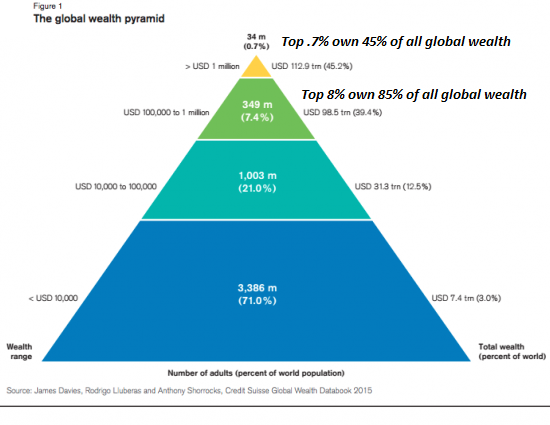

The benefits of these financial instruments were asymmetric: those originating these instruments made billions, while the borrowers taking on the subprime mortgages, etc. were accepting risks they didn't understand. This dynamic fueled soaring wealth/income inequality.

Apparently unbeknownst to central bankers, super-low interest rates and abundant liquidity didn't spur investments in increasing productivity, it incentivized highly leveraged speculative bets. This manifested in subprime mortgages funding house-flipping by the masses and the origination of exotic financial instruments such as CDOs and CLOs.

Ultimately, the central banks' no-holds-barred Neoliberalism led to the Global Financial Crisis (GFC) of 2008-09, as the risks that were supposedly hedged blew up and the markets froze up (i.e. markets became illiquid as buyers vanished).

As former Fed Chair Alan Greenspan admitted, the central banks failed to see that markets are not as self-regulating as the Neoliberal faithful believed: when bubbles pop, buyers vanish and markets go bidless/illiquid: sellers are desperate to sell but there are no buyers at any price.

This was the inevitable end-game of financialized, globalized Neoliberalism, and rather than face that reality, central banks and policy-makers double-downed on the same policies that created the 2008 bubble that was destined to pop with horrific consequences to everyone who had a stake in any of the casino's games.

We now come to the 2010s, in which financialization and globalization essentially conquered the global economy, leading to the brittle fragilities that are now unraveling.

With the cost of living rising and wages stagnating, the "solution" was to borrow $10 to get $1 of growth. Since global markets were saturated with debt and risk, lenders cannibalized domestic markets, loading college students with $2 trillion in student loans and enabling a fracking "miracle" that was less an energy miracle and more a financial miracle as companies that lost billions continued to get cheap loans and sell bonds.

The global economy is now teetering on a precipice in every sector: energy extraction costs have risen, requiring higher prices for oil, but consumers whose wages have stagnated for 20 years can no longer afford higher prices for oil or anything else.

Globalization has optimized profits at the expense of everything else: ecological sustainability, the security of food and energy sources, etc., while financialization has gutted the real economy in an extraction process that concentrates all the gains into the hands of the few at the top of the financialization/globalization pyramid: a winners-take-most economy that has corrupted and distorted the political and social orders.

All the critical dynamics--energy, currencies, globalization, debt and financialization--have reached extremes that made destabilization--i.e. a tumble into collapse--inevitable.

What happens when the naive hope that the brittle, fragile extremes of the global economy could be completely restored to mid-2019 levels dissipates and is replaced by the sober realization there not only will there not be a recovery, but there can't be a recovery, as those brittle extremes have been lost for good?

Since the authorities have no Plan B, uncertainty, risk and volatility could reach extremes few anticipate as Plan A--push extremes to even riskier extremes--generates increasingly consequential unintended consequences.

The unstable, brittle edge of the precipice is giving way, and there is nothing but air below.

Recent Podcasts:

Audiobook edition now available:

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 (Kindle), $12 (print), $13.08 ( audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print) Read the first section for free (PDF).

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Robert E. ($500), for your beyond-outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, William S. ($50), for your superbly generous contribution to this site -- I am greatly honored by your support and readership. |