The value of these super-abundant follies will trend rapidly to zero once margin calls and other bits of reality drastically reduce demand.

Inflation, deflation, stagflation–they’ve all got proponents. But who’s going to be right?The difficulty here is that supply and demand are dynamic and so there are always things going up in price that haven’t changed materially (and are therefore not worth the higher cost) and other things dropping in price even though they haven’t changed materially.

So proponents of inflation and deflation can always offer examples supporting their case.The stagflationist camp is delighted to offer a compromise case: yes, there are both deflationary and inflationary dynamics, and what we have is the worst of both worlds: stagnant growth and declining purchasing power.

What’s missing in most of these debates is a comparison of scale: deflationists point to things like big-screen TV prices dropping. OK, fine: we save $300 on a TV that we might buy once every two or three years. So we save $100 a year thanks to this deflation.

Meanwhile, on the inflationary side, healthcare insurance went up $3,000 a year, childcare went up $3,000 a year, rent (or property taxes) went up $3,000 a year and care for an elderly parent went up $3,000 a year: that’s $12,000. Now how many big-screen TVs, shoddy jeans, etc. that dropped a bit in price will we have to buy to offset $12,000 in higher costs?

This is the problem with abstractions like statistics: TVs dropped 20% in cost, while healthcare, childcare, assisted living and rent all went up 20%–so these all balance out, right?

There are two glaring omissions in all the back-and-forth on inflation and deflation:

1. Price is set on the margins.

2. Enterprises cannot lose money for very long and so they close down.

Let’s start with an observation about the dynamics of price/cost: supply and demand. As a general rule, things that are scarce and in high demand will go up in price, and things that are abundant and in low demand will drop in price.

Whatever is chronically scarce and necessary for life will have a ceaseless pressure to cost more, whatever is abundant and no longer desirable will have a ceaseless pressure to cost less.

Now we come to the overlooked mechanism #1: Price is set on the margins. Housing offers an example: take a neighborhood of 100 homes. The five sales last year were all around $600,000, and so appraisers set the value of the other 95 homes at $600,000.

Things change and the next sale is at $450,000. This is dismissed as an outlier, but then the next two sales are also well below $500,000. By the fifth sale at $450,000, the value of each of the 95 homes that did not change hands has been reset to $450,000. The five houses that traded hands set the price of the 95 houses that didn’t change hands. Price is set on the margins.

The biggest expense in many enterprises and agencies is labor. Those who own enterprises know that it’s not just the wage being paid that matters, it’s the labor overhead: the benefits, insurance and taxes paid on every employee. These are often 50% or more of the wages being paid. These labor overhead expenses have skyrocketed for many enterprises and agencies, increasing their labor costs in ways that are hidden from the employees and public.

It’s important to recall that roughly 3/4 of all local government expenses are for labor and labor overhead–healthcare, pensions, etc. Where do you think local taxes are heading as labor and labor-overhead costs rise? What happens to pension funds when all the speculative bubbles all pop?

The cost of labor is also set on the margins. The wage of the 100-person workforce is set by the five most recent hires, and if wages went up 20% to secure those employees, the cost of the labor of the other 95 workers also went up 20%. (Employers can hide a mismatch but not for long, and such deception will alienate the 95% who are getting paid less for doing the same work.)

Labor is scarce for fundamental reasons that aren’t going away:

1. Demographics: large generation is retiring, replacements are not guaranteed.

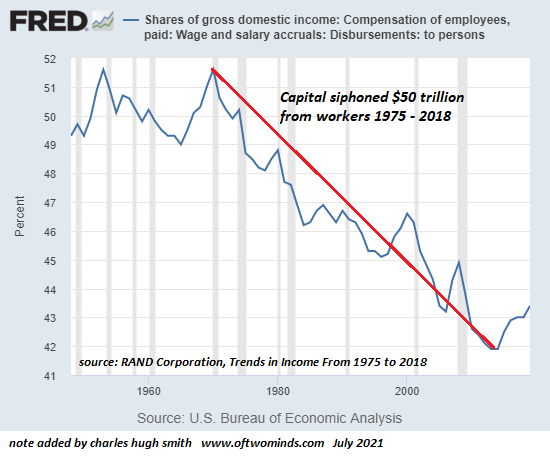

2. Catch-up: labor’s share of the economy has declined for 45 years. Now it’s catch-up time.

3. Cultural shift in values: Antiwork, slow living, FIRE–all are manifestations of a profound cultural shift away from working for decades to pay debts and enrich billionaires to downshifting expenses and expectations in favor of leisure and agency (control of one’s work and life).

4. Long Covid and other chronic health issues: whether anyone cares to admit it or not, Long Covid is real and poorly tracked. A host of other chronic health issues resulting from overwork, stress and unhealthy lifestyles are also poorly tracked. All these reduce the supply of labor.

5. Competing demands of family and work. Work has won for 45 years, now family is pushing back.

Put these together–diminishing supply of labor and labor being priced on the margins–and you get a runaway freight train of higher labor costs. Add in runaway increases in labor overhead and you’ve got a runaway freight train with the throttle jammed to 11.

Deflationists make one fatally unrealistic assumption: that enterprises facing sharply higher costs for labor, components, shipping, taxes, etc. will continue making big-screen TVs, shoddy jeans, etc. even as the price the products and services fetch plummets below the costs of producing them.

The wholesale price of the TV can’t drop below production and shipping costs for very long. Then the manufacturers close down production and the over-abundance of TVs, etc. goes away. Nation-states can subsidize production of some things for a time, but selling at a loss is not a long-term winning strategy: subsidizing failing enterprises and money-losing state-owned companies is a form of malinvestment that bleeds the economy dry.

The only thing that will still be super-abundant as demand plummets is phantom-wealth “investments”, i.e. skims, scams, bubbles and frauds. The value of these super-abundant follies will trend rapidly to zero once margin calls and other bits of reality drastically reduce demand.

Real-world costs: much higher. Speculative gambles: much lower. As in zero.

Thank you, everyone who dropped a hard-earned coin in my begging bowl this week–you bolster my hope and refuel my spirits.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Recent Videos/Podcasts:

Bit About Crypto Podcast – Charles Hugh Smith (58 min)

My recent books:

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic($5 (Kindle), $10 (print), (audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake$1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print)Read the first section for free (PDF).

Become a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, Gavin G. ($50), for your marvelously generous contribution to this site — I am greatly honored by your support and readership. | Thank you, August M. ($20), for your much-appreciated generous contribution to this site — I am greatly honored by your support and readership. |

| Thank you, Tim K. ($52), for your superbly generous contribution to this site — I am greatly honored by your support and readership. | Thank you, Alex T. ($50), for your splendidly generous contribution to this site — I am greatly honored by your support and readership. |