I like a rousing story as much as anyone else, but systems aren’t stories, and confusing the two won’t actually fix what’s not sustainable in the current system’s configuration.

OK, I get it: we all like Hollywood endings: the superhero saves the world, the evil conspiracy is uncovered and the villains get their just desserts and the impossible romance overcomes all the odds. This is why there are Hollywood endings: we are hard-wired to thrill to happy endings and a successful conclusion to the Hero’s / Heroine’s Journey.

We will tolerate a Tragic Hero / Heroine or the occasional Anti-Hero / Heroine, but there is still a moral victory of some sort to cheer.

The real world doesn’t follow a storyline, it operates according to the dictates of systems: inputs are taken up by processes which then generate outputs. If the outputs and processes don’t change, the outputs don’t change either.

One prevalent manifestation of human hubris is the idea that getting someone to agree with us about something or other is some sort of victory, as if human opinions matter. They don’t, unless they change either inputs or processes in extremely consequential ways. Tweaking inputs or policies might make us feel warm and fuzzy (“I’m part of the solution!”) but they are too modest to change the system’s inputs and processes. The net result is the outputs remain the same.

Put another way: labeling something or other a hoax or an existential threat doesn’t change anything in the systems that generate consequences. Whatever is going to happen as output is going to happen regardless of what humans label it or their opinions about it (“El Nino really sucks!”).

Existing processes constrain our choices. This is why it’s difficult to be an environmentally-sustainable saint. Let’s say we’re concerned about climate change and the destruction of the planet’s biosphere. Let’s say we want to lower our carbon footprint and “do the right things” to reduce the negative impact of our consumption and lifestyle.

This is where we substitute Hollywood endings for reality. We like to think that recycling matters. Sorry, it really doesn’t change the inputs or processes enough to change the outputs in any consequential way. For example, the percentage of lithium batteries and electronic waste that are currently recycled is near-zero because the batteries and electronics aren’t manufactured to be recycled in a cost-effective manner, and nobody in the system pays for costly recycling. So the really important recycling isn’t being done.

I still recycle cardboard because that seems like a better choice than dumping it in the landfill, but in terms of total lifecycle costs and resource consumption of recycling versus landfill, I don’t have any data. The system isn’t set up to measure total lifecycle costs and resource consumption of goods, services and processes, and since we only manage what we measure, we’re flying blind: the system is set up to measure “growth” (GDP) and profits, not total lifecycle costs and resource consumption.

Sorry, there’s no Hollywood ending until we change the inputs (stop manufacturing lithium batteries) and/or the processes (require 99% recycling of all electronics, batteries, vehicles, etc.). This will require changing the entire manufacturing and resource supply chain systems from the ground up, globally. If we don’t do that, the output can’t possibly change in any consequential way.

The Hollywood ending is electric vehicles will “save the planet.” Too bad this is Hollywood, not reality. Most of the consumption of resources and damage to the planet occur in the mining, smelting and manufacture of the vehicle, regardless of its fuel. Due to their massive consumption of minerals, electric vehicles consume far more of the planet’s resources than an ICE (internal combustion engine) vehicle.

All vehicles are manufactured (mining, smelting, transport, factories, etc.) with hydrocarbons. There’s no difference between vehicles except electric vehicles use even more hydrocarbons in their fabrication.

Then there’s the source of the fuel. An electric vehicle manufactured by burning coal and charged with electricity generated by burning coal is in fact a coal-burning vehicle. Calling it “electric” fits the happy story, but it’s not actually factual: a coal-burning vehicle is an environmental disaster, regardless of labels, our opinions or the happy-ending PR.

In the real world, the least destructive choice of vehicle is a small, light, old ICE vehicle that is well-maintained to conserve fuel and driven only rarely. Hey, look at me, I only drove my old 40-mile-per-gallon Civic 3,000 miles last year–I’m a saint!

Unfortunately, the real world isn’t a Hollywood (or Bollywood) movie, and so I don’t get to be a saint once we look at the world as a system rather than a movie. The fertilizers I use to grow food in my yard come from afar, and even the organic ones consume huge quantities of hydrocarbons in their processing, bagging and shipping. The “organic” fruit or vegetable shipped from afar is an environmental disaster compared to the organic fruit or vegetable from your own yard, but even those require inputs that are part of the system.

I stepped on airliners a few times in the past year, one long-haul and two short flights, and there is really nothing environmentally saintly about consuming immense resources by jetting around the world.

Electric aircraft won’t “save the world,” either. They’re resource-hungry, small, slow, their range is modest and their batteries are no more recyclable or long-lasting than all the vehicle batteries destined for the landfill. And alternative fuels for jet aircraft are incapable of being produced at the scale necessary to replace jet fuel. Sorry, no Hollywood ending.

To really reduce one’s consumption of the planet’s resources, we would have to grow our own food, get around on our own feet or zero-fuel transport (motorless bicycle or skateboard or boat) and not buy / own / use large resource-consuming devices such as vehicles, aircraft, etc.

The system as currently configured makes it nearly impossible to do this. Even growing much of your own food requires delivery of fertilizers (organic or chemical, they still weight a lot). Very few places are bike-skateboard friendly. The world is set up for large, mass-produced fueled vehicles. Outside of a few cities, public transport is incapable of getting people where they need to go in any sort of time-efficient manner.

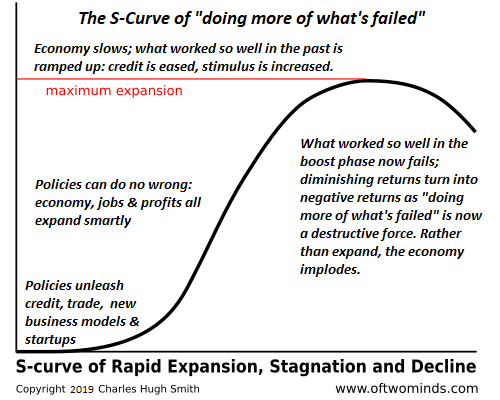

Consider the foundation of our lifestyle, the financial system. The story is “debt doesn’t matter,” because we can outgrow rising debt forever. Our bag of financial engineering tricks is bottomless, and there will always be another financial rabbit we can pull out of the hat.

This is of course a fantasy. Debt eventually eats the system alive. So do fixed costs, entitlements, demographics and declining productivity. The inputs and processes can’t be changed in any material way because they have to remain in their current scale and configuration or the financial system collapses under its own weight.

This brings us to the incentives to keep the inputs and processes exactly as they are, with minor tweaks for PR purposes. The system is set up such that elites and self-serving interests have most of the wealth and political power, and if even the tiniest bit of their skim is diminished, they will instantly devote the entirety of their resources to reversing this outrage, for they all know how power works: if others manage to cut 1% from your skim, they’ll sense weakness and come back for 10%.

The only incentive that counts in our stripmined world is maximizing profits and the private gains of the entrenched and powerful. To cloak this reality, the Powers That Be promote public-relations propaganda that depicts their pillage, looting, fraud and destruction as a Hollywood story we can all consume and love, just as we love our servitude once it’s been properly packaged into a Hero / Heroine’s Journey or a Love Story.

This is why nobody will do anything until it’s too late. It’s only when we run out of essential inputs and/or essential processes decay and collapse that we’ll awaken to the fact that since the global system’s inputs and processes materially changed, the outputs we need and love all went away.

By the time inputs and processes have materially changed, it’s too late to reverse the process and go back in time.

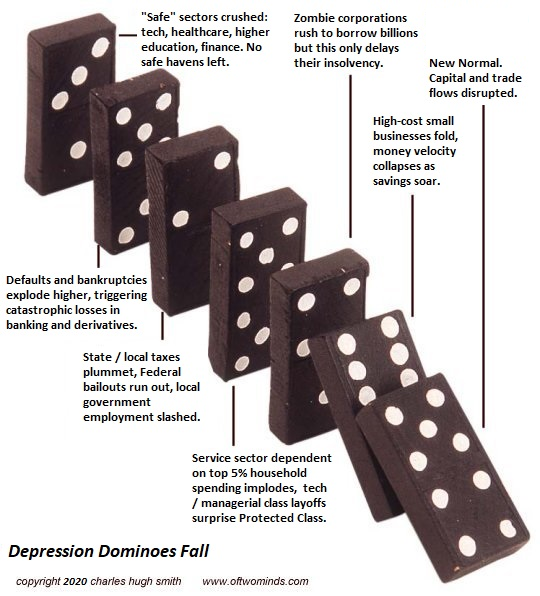

Once resource extraction processes break down, inputs are no longer available in the needed quantities to feed all the processes of globalized, industrialized production and transport. Since all these processes are tightly bound systems, that is, interconnected, the breakdown of any one supply chain or process quickly topples dominoes throughout the system.

In addition to confusing happy stories with systems, human hubris manifests in another way: we like to think that minor tweaks here and there that don’t inconvenience us will magically change the negative outputs (resource depletion, environmental ruin, etc.). This is why we love the Hollywood stories about electric aircraft (our very own electric helicopter–yowza!), electric vehicles, recycling the carboard boxes from FedEx, UPS and Amazon, and so on: we get all the comforts and conveniences we’re accustomed to, and we get to be environmentally-sustainable saints, too: it’s all sustainable and ecological and warm and fuzzy.

Except it isn’t. That’s a fairy tale, not a system.

If you question the Hollywood ending, you’re dismissed as a doom and gloomer, a discontent who grumbles about happy endings and techno-marvels.

I see this as confusing a story with a system. The story operates by its own rules: here are the obstacles and powerful villains, here are the Hero and Heroine, outmatched and under pressure, but then, against all odds, the villains lose their grip, justice is served and love triumphs.

Systems work by their own implacable rules. There are inputs and processes that generate outputs. The only way to change the outputs in a consequential fashion is to change the inputs and/or processes in a consequential fashion. Little face-saving PR tweaks are too small in scale to materially change either inputs or processes, and so the outputs won’t change and indeed, can’t possibly change, because that’s how systems work.

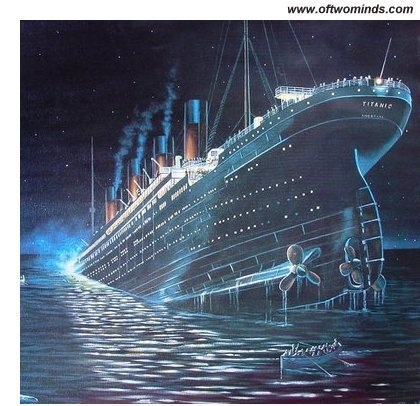

So by all means, ignore all warnings and run the ship at full speed through an ice field. All too predictably, the ship collides with an iceberg and only then does anyone respond: OK, where’s the Hollywood story of brave engineers saving the ship and noble passengers helping each other onto lifeboats? What do you mean, the ship will sink regardless of what’s done?

Doesn’t our happy-ending story map reality? Unfortunately, no. The current system is sinking and nobody will do anything other than more of what’s failed until it’s too late.

I like a rousing story as much as anyone else, but systems aren’t stories, and confusing the two won’t actually fix what’s not sustainable in the current system’s configuration.

This confusion of story with system will generate consequences and opportunities which I discuss in my books

Global Crisis, National Renewal

and

Self-Reliance in the 21st Century.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Paul C. ($300), for your beyond-outrageously generous contribution

to this site — I am greatly honored by your steadfast support and readership.

|

|

Thank you, Julius L. ($50), for your magnificently generous contribution

to this site — I am greatly honored by your support and readership.

|

|

Thank you, Michael T. ($35), for your superbly generous contribution

to this site — I am greatly honored by your steadfast support and readership.

|

|

Thank you, Sarah S. ($1/month), for your most generous pledge

to this site — I am greatly honored by your support and readership.

|

New Podcast:

Its a Waterfall - Risk, Collateral & Productivity (48 min)

New Podcast:

Its a Waterfall - Risk, Collateral & Productivity (48 min)